Data Services

Data Services Deutsch

Deutsch Español

Español Français

Français Italiano

Italiano Nederlands

Nederlands Polski

Polski USA

USAThe Acquis Index shares the trends that Acquis is witnessing in equipment leasing volumes which may prove a useful indicator for emerging trends in the wider leasing industry.

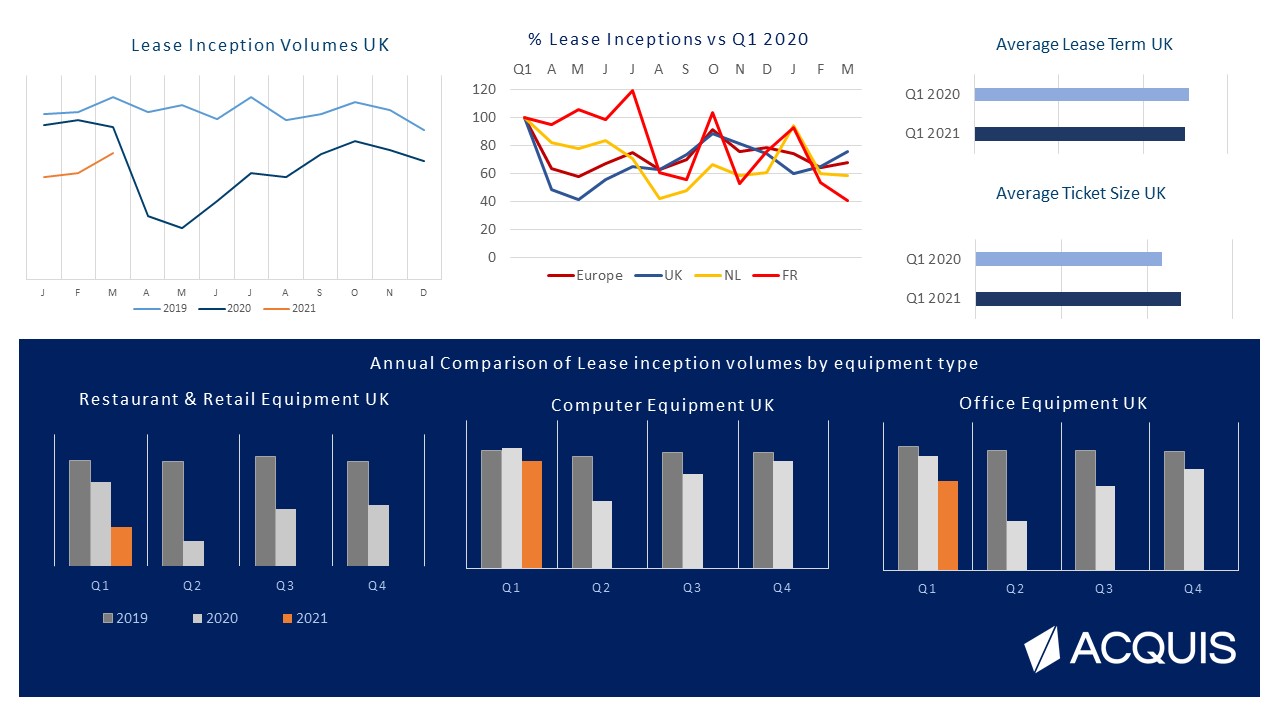

The first full quarter of 2021 saw wide divergence between different European countries in terms of lease volumes. This was to be expected, as a third wave of the pandemic hit different regions at different times, and the timing of reinstated lockdowns varied across regions. Q1 2021 saw a continued downward trajectory for most European countries in the survey when compared to volumes in the first quarter of last year before the pandemic hit, with France experiencing the largest comparative downturn in lease inceptions fuelled by a third wave and strict lockdowns during the period. The picture for the UK however is somewhat brighter, as the only country in the survey to regain volume during Q1 when compared to the previous quarter.

Click here to view the Acquis Index Q1 2021 graphs.

{kind=link}

While lease inceptions are still tracking at around 25% below 2019 volumes in the UK, we are beginning to see positive signs of a more stable recovery trend across all equipment classes, no doubt related to the rapid deployment of the UK’s vaccination programme and, to date, the avoidance of a third wave. Q2 2021 should see this positive trend ripple out across Europe as vaccination programmes are widely deployed improving consumer confidence and allowing society to reopen.

A look at equipment classes reveals computer equipment in the UK is almost back to pre-pandemic volumes. Office equipment continues to lag behind both this time last year and 2019, a dip possibly deepened by large scale office closures and adoption of work from home flexibility. Restaurant equipment remains one of the most deeply affected categories still only at a third of the volumes it was achieving in 2019.

Some trends we might have anticipated in the data as a result of current market conditions would be that average lease terms may begin to creep up as customers look to spread the cost of borrowing, and average ticket size may reduce, possibly as a result of a move to mobile working. However, to date neither of these trends have transpired in the data for the UK; indeed, both measures are currently leaning away from this prediction, which shows the recovery market is still unpredictable and it remains to be seen what after-effects will persist long term.

Acquis’ Chief Commercial Officer, James Rudolf, comments, “The end of Q1 feels like the end of a long, hard winter in the UK as people begin to emerge from months of lockdowns, yet this isn’t necessarily reflected in the data, which for the UK market is already on a positive recovery trend. The road ahead is by no means clear, however, as government coronavirus loan schemes come to an end and concerns over virus variants remain a reality, but yet again we are seeing signs of resilience in the leasing industry, and from talking to our clients, the industry feels well poised to lead the recovery and bounce back strongly.”

ABOUT THE INDEX: As an independent insurance administrator working in partnership with over 100 leasing companies across 14 European countries, Acquis has been providing specialist insurance programmes for equipment leasing for over a decade, and during the course of this time our management data has proved to be a reliable early indicator of changes in new business volumes across the leasing industry.

Acquis’ own volumes are predominantly made up of small ticket equipment with an average ticket size of €13,000. 58% of the volumes are made up of IT / office equipment, 15% retail and 12% manufacturing, with the remainder consisting of construction, material handling, medical and other assets.